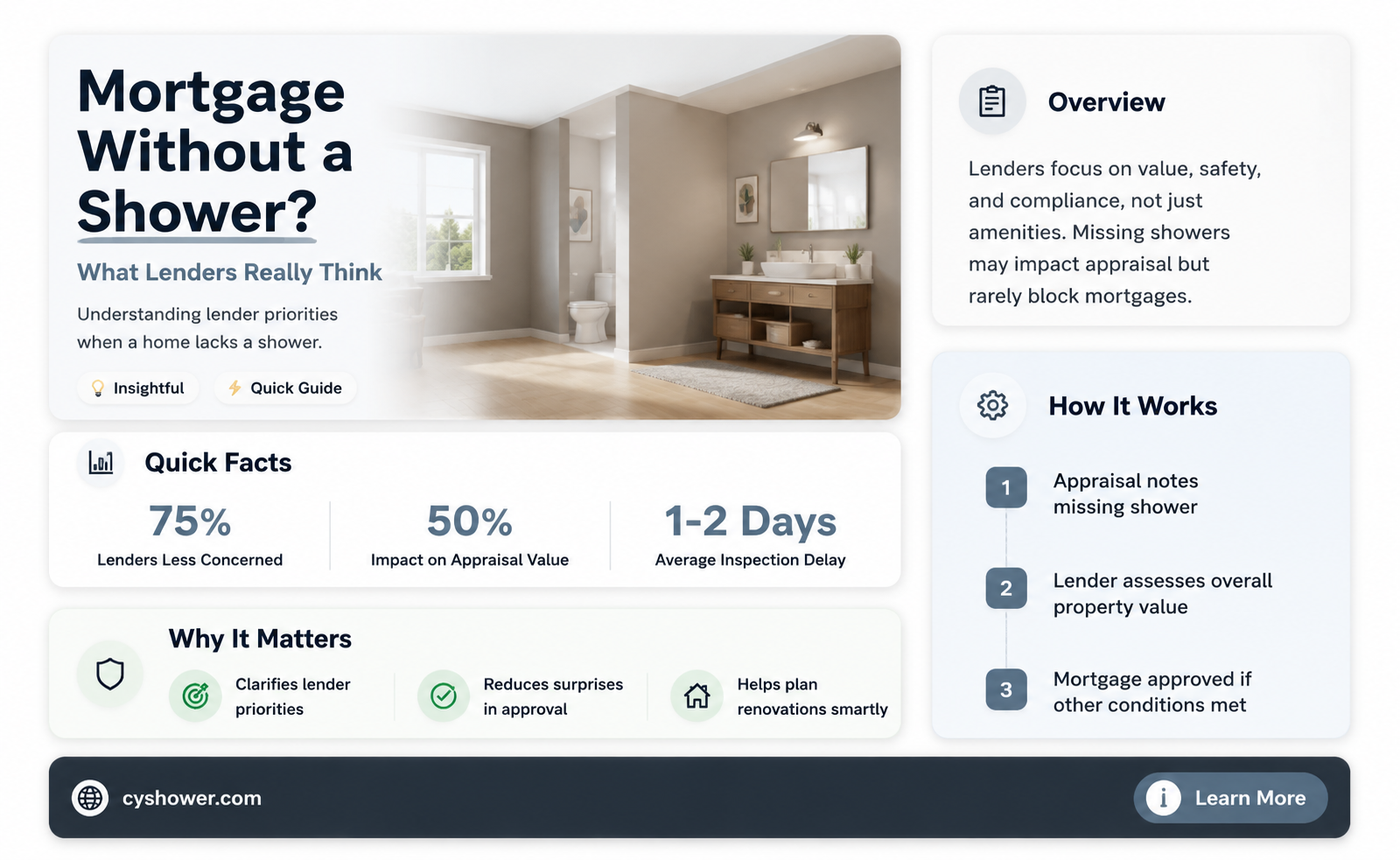

When considering whether you can get a mortgage with no shower, it's essential to understand that lenders primarily focus on the property's overall condition, value, and habitability. While a shower is a standard feature in most homes, its absence doesn’t automatically disqualify you from obtaining a mortgage. However, lenders may view the lack of a shower as a potential issue, as it could affect the property’s marketability and value. Some lenders might require the installation of a shower before approving the loan, while others may proceed but at a lower loan-to-value ratio or with additional conditions. Additionally, local building codes and regulations may mandate certain amenities, including a shower, which could further complicate the process. Therefore, addressing this issue before applying for a mortgage is crucial to ensure a smoother approval process.

| Characteristics | Values |

|---|---|

| Lender Requirements | Most lenders require properties to meet minimum habitability standards, which often include a functional bathroom with a shower or bathtub. |

| Appraisal Impact | A property without a shower may appraise lower, affecting loan approval or amount. |

| Loan Types | Conventional loans are less likely to approve; government-backed loans (FHA, USDA, VA) may have more flexibility but still require basic habitability. |

| Renovation Loans | Options like FHA 203(k) or Fannie Mae HomeStyle allow borrowing for repairs, including adding a shower. |

| Rural Properties | Some lenders may be more lenient for rural properties, but standards still apply. |

| Temporary Solutions | Lenders may accept temporary solutions (e.g., portable showers) if a permanent fix is planned. |

| Local Building Codes | Compliance with local codes is mandatory; lack of a shower may violate regulations. |

| Impact on Saleability | Properties without a shower may be harder to sell, affecting mortgage approval. |

| Lender Discretion | Approval ultimately depends on the lender’s policies and risk assessment. |

| Alternative Options | Consider personal loans or cash for renovations if mortgage approval is denied. |

Explore related products

What You'll Learn

- Minimum Property Standards: Lenders require homes to meet basic living standards, including functional bathrooms

- Appraisal Challenges: Lack of a shower can lower property value and appraisal, affecting loan approval

- Renovation Loans: Options like FHA 203(k) allow financing for necessary home improvements, including showers

- Alternative Bathing Solutions: Temporary fixes like portable showers may not satisfy lender requirements

- Lender Discretion: Some lenders may approve loans if other factors (e.g., equity) are strong

![]()

Minimum Property Standards: Lenders require homes to meet basic living standards, including functional bathrooms

Lenders aren't in the business of funding substandard housing. Minimum Property Standards (MPS) exist to protect both borrowers and lenders by ensuring homes meet basic health, safety, and habitability requirements. These standards, often aligned with FHA guidelines, mandate functional bathrooms as a cornerstone of livability. A missing shower isn't just an inconvenience; it's a red flag signaling potential structural issues, sanitation concerns, or neglect.

Why Spiders Invade Showers: Uncovering the Surprising Reasons Behind the Creepy Crawlers

You may want to see also

Explore related products

![]()

Appraisal Challenges: Lack of a shower can lower property value and appraisal, affecting loan approval

A property without a shower can face significant appraisal challenges, directly impacting its value and mortgage approval odds. Appraisers assess a home’s condition, functionality, and marketability, and the absence of a shower raises red flags in all three areas. Lenders rely on appraisals to determine loan-to-value ratios, and a lower appraisal can result in reduced loan amounts or outright denials. For instance, a home lacking a shower might appraise 10-15% below comparable properties, forcing buyers to either cover the gap in cash or walk away from the deal.

Consider the practical implications for buyers and sellers. A property without a shower often appeals to a narrower market, typically investors or those willing to renovate. This limited pool of buyers can suppress the sale price, further complicating the appraisal process. Appraisers may struggle to find comparable properties, leading to conservative valuations. For lenders, this uncertainty increases risk, prompting stricter underwriting standards or higher interest rates. Sellers might need to invest in upgrades before listing, while buyers could face delays or additional costs to secure financing.

From a lender’s perspective, a property without a shower represents a non-conforming asset. Mortgage guidelines often require homes to meet minimum habitability standards, which include basic amenities like a functional bathroom. FHA loans, for example, mandate that properties have a bathtub or shower in at least one bathroom. Failure to meet these standards can disqualify a home from certain loan programs, limiting financing options. Even if a lender approves the loan, they may require escrow holdbacks for renovations, adding complexity to the transaction.

To mitigate these challenges, proactive steps are essential. Sellers should consider installing a shower before listing, as the investment often yields a higher sale price and smoother appraisal. Buyers can negotiate repairs or price reductions to account for the deficiency. Working with experienced real estate agents and lenders who understand appraisal nuances can also help navigate potential roadblocks. For unconventional properties, alternative financing options like renovation loans (e.g., FHA 203k) may provide a viable solution, though they come with additional requirements and costs.

In summary, the absence of a shower is more than a cosmetic issue—it’s a critical factor in property valuation and mortgage approval. Addressing this deficiency upfront can prevent appraisal setbacks and expand financing opportunities. Whether you’re buying or selling, understanding these challenges and taking strategic action can make all the difference in securing a successful transaction.

Effective Ways to Remove Stubborn Shower Glass Stains Easily

You may want to see also

Explore related products

![]()

Renovation Loans: Options like FHA 203(k) allow financing for necessary home improvements, including showers

A home without a shower can be a deal-breaker for many buyers, but it doesn’t have to derail your mortgage plans. Renovation loans, such as the FHA 203(k) program, are specifically designed to finance both the purchase of a home and the cost of necessary improvements, including installing a shower. This loan rolls the purchase price and renovation costs into a single mortgage, eliminating the need for separate financing. For buyers eyeing fixer-uppers or homes lacking modern amenities, this option bridges the gap between affordability and livability.

To qualify for an FHA 203(k) loan, the property must be at least one year old, and the renovation costs must exceed $5,000. The loan covers a wide range of improvements, from structural repairs to cosmetic upgrades, making it ideal for addressing essential features like showers. Borrowers must work with an FHA-approved lender and hire a HUD consultant to assess the renovation scope and costs. While the process involves more paperwork than a traditional mortgage, it’s a practical solution for homes that need significant updates to meet modern standards.

One of the standout benefits of the FHA 203(k) loan is its flexibility. Unlike traditional mortgages, which require the home to be in move-in condition, this program allows buyers to tackle improvements immediately. For instance, if a home lacks a shower, the loan can cover the installation of plumbing, fixtures, and tiling, ensuring the property meets basic living requirements. This not only enhances the home’s functionality but also increases its value, making it a smart investment for long-term homeowners.

However, borrowers should be aware of the program’s limitations. The FHA 203(k) loan has strict guidelines regarding eligible improvements, and luxury upgrades like high-end fixtures may not qualify. Additionally, the loan requires a minimum credit score of 580 and a down payment of at least 3.5%, though this can vary based on the lender. Prospective buyers should also factor in the time and effort required for renovations, as delays can impact the overall timeline and budget.

In conclusion, renovation loans like the FHA 203(k) offer a viable solution for buyers facing homes without essential features like showers. By combining purchase and improvement costs into one loan, this program removes barriers to homeownership and empowers buyers to transform properties into comfortable, modern living spaces. While the process demands careful planning and adherence to guidelines, the end result is a home tailored to the buyer’s needs and a solid investment for the future.

Shower Surprise: Why Do You Pee When You Get In?

You may want to see also

Explore related products

![]()

Alternative Bathing Solutions: Temporary fixes like portable showers may not satisfy lender requirements

Lenders often require homes to have permanent, functional bathing facilities to approve a mortgage. Temporary solutions like portable showers, camping showers, or gym memberships might seem practical for personal hygiene, but they rarely meet lender standards. These alternatives lack the permanence and integration into the home’s plumbing system that lenders seek. For instance, a portable shower bag hanging from a tree in the backyard or a gym shower 10 miles away doesn’t equate to a fixed, in-home bathing solution in a lender’s eyes. Understanding this distinction is critical if you’re considering purchasing a property without a traditional shower.

From a practical standpoint, installing a temporary bathing solution involves minimal effort but offers limited long-term value. Portable showers, such as battery-operated units or solar-heated bags, cost between $20 and $200 and can be set up in under an hour. However, these options often lack temperature control, water pressure, and privacy, making them less appealing for daily use. Similarly, relying on external facilities like public showers or a neighbor’s bathroom introduces inconvenience and uncertainty. While these fixes might suffice for short-term living, they do not address the lender’s requirement for a permanent, in-home solution.

Persuasively, it’s worth noting that lenders view permanent fixtures as indicators of a property’s value and habitability. A home without a shower may be deemed substandard, potentially reducing its appraisal value or disqualifying it from certain loan programs. For example, FHA loans require homes to meet minimum property standards, including functional bathing facilities. Even if you plan to install a shower post-purchase, lenders typically require proof of completion before closing. Temporary solutions, no matter how innovative, fail to bridge this gap, leaving you at risk of loan denial or higher interest rates.

Comparatively, alternative bathing solutions like wet rooms, clawfoot tubs with handheld showerheads, or even outdoor showers with proper plumbing can be more lender-friendly. These options, while not traditional, integrate into the home’s infrastructure and demonstrate a commitment to meeting basic living standards. For instance, a wet room—a fully waterproofed bathroom without a shower curtain—costs between $5,000 and $10,000 to install but aligns more closely with lender expectations than a portable camping shower. Such permanent upgrades not only satisfy lenders but also enhance the property’s long-term value.

In conclusion, while temporary bathing solutions offer immediate relief, they fall short of lender requirements for mortgage approval. If you’re considering a property without a shower, prioritize permanent, integrated solutions to ensure both personal comfort and financial feasibility. Temporary fixes may be a stopgap, but they’re no substitute for the permanence lenders demand.

Effective Ways to Eliminate Annoying Shower Flies for Good

You may want to see also

Explore related products

![]()

Lender Discretion: Some lenders may approve loans if other factors (e.g., equity) are strong

Lenders often wield significant discretion when evaluating mortgage applications, and the absence of a shower in a property doesn’t automatically disqualify a borrower. Instead, lenders may focus on other mitigating factors, such as the borrower’s equity position. For instance, if a borrower has a substantial down payment—say, 30% or more of the property’s value—this can offset concerns about the property’s condition. High equity reduces the lender’s risk, as it provides a larger buffer against potential losses if the property needs to be sold. This approach allows lenders to balance risk while still approving loans for properties that might otherwise be considered substandard.

Consider a scenario where a borrower seeks a mortgage for a fixer-upper without a shower. If the borrower has excellent credit, stable income, and a 40% down payment, a lender might approve the loan despite the property’s shortcomings. The lender’s rationale? The borrower’s strong financial profile and significant equity minimize the risk of default. Additionally, the lender may recognize that the borrower intends to renovate the property, potentially increasing its value over time. This flexibility highlights how lender discretion can work in the borrower’s favor when other factors are compelling.

However, borrowers should be aware that not all lenders apply discretion equally. Traditional banks may adhere strictly to underwriting guidelines, rejecting properties without essential amenities like a shower. In contrast, credit unions, private lenders, or portfolio lenders—those who keep loans in-house rather than selling them—may be more willing to consider individual circumstances. For example, a local credit union might approve a mortgage for a property without a shower if the borrower has a long-standing relationship with the institution and a history of financial responsibility. Researching lender-specific policies and cultivating relationships with flexible institutions can increase the chances of approval.

To maximize the likelihood of securing a mortgage under these conditions, borrowers should focus on strengthening their application in other areas. This includes maintaining a high credit score (740 or above), reducing debt-to-income ratios to below 36%, and providing detailed plans for property improvements. For instance, presenting a contractor’s estimate for installing a shower and other renovations can reassure lenders of the property’s future value. Borrowers should also be prepared to negotiate terms, such as accepting a slightly higher interest rate or providing additional collateral, to compensate for the property’s current deficiencies.

Ultimately, lender discretion offers a pathway to mortgage approval for properties lacking essential features like a shower, but it requires borrowers to demonstrate exceptional strength in other areas. By focusing on equity, creditworthiness, and a clear plan for improvement, borrowers can position themselves as low-risk candidates despite the property’s condition. This approach not only increases the chances of approval but also aligns with lenders’ interests in funding loans that are likely to perform well over time. Borrowers should view this as an opportunity to showcase their financial resilience and vision for the property’s potential.

Shower Struggles: Why You Might Still Feel Dirty After Washing

You may want to see also

Frequently asked questions

It’s unlikely. Most lenders require properties to meet minimum habitability standards, which typically include a functioning bathroom with a shower or bathtub.

It depends on the lender and the property’s overall condition. Some may approve it if the bathtub is in good condition, but others may require a shower installation before closing.

Most lenders won’t approve a mortgage if the property doesn’t meet habitability standards at the time of purchase. You may need to install the shower before closing or explore renovation loans.

Some renovation loans, like FHA 203(k) or Fannie Mae HomeStyle, may allow you to finance shower installation, but the property must still meet basic habitability requirements.

Failing to disclose this could lead to loan denial or legal issues. Lenders conduct appraisals and inspections, so the lack of a shower will likely be discovered.

![House (The Criterion Collection) [Blu-ray]](https://m.media-amazon.com/images/I/7121e6-w-AL._AC_UL320_.jpg)